Using a Health Savings Account (HSA) to Pay for Childbirth

Welcoming a new child is great, but pricey. Even if you’re blessed to have a birth with no complications, the bill is still hefty to cover what insurance does not. A bit of planning can help reduce your family’s stress around this cost and help you focus on your new family member. An HSA can go a long way to help with this effort. Keep reading for how to use this unique health care account to help with this momentous event.

"Behold, children are a heritage from the LORD, the fruit of the womb a reward." Psalm 127:3 ESV

What is an HSA?

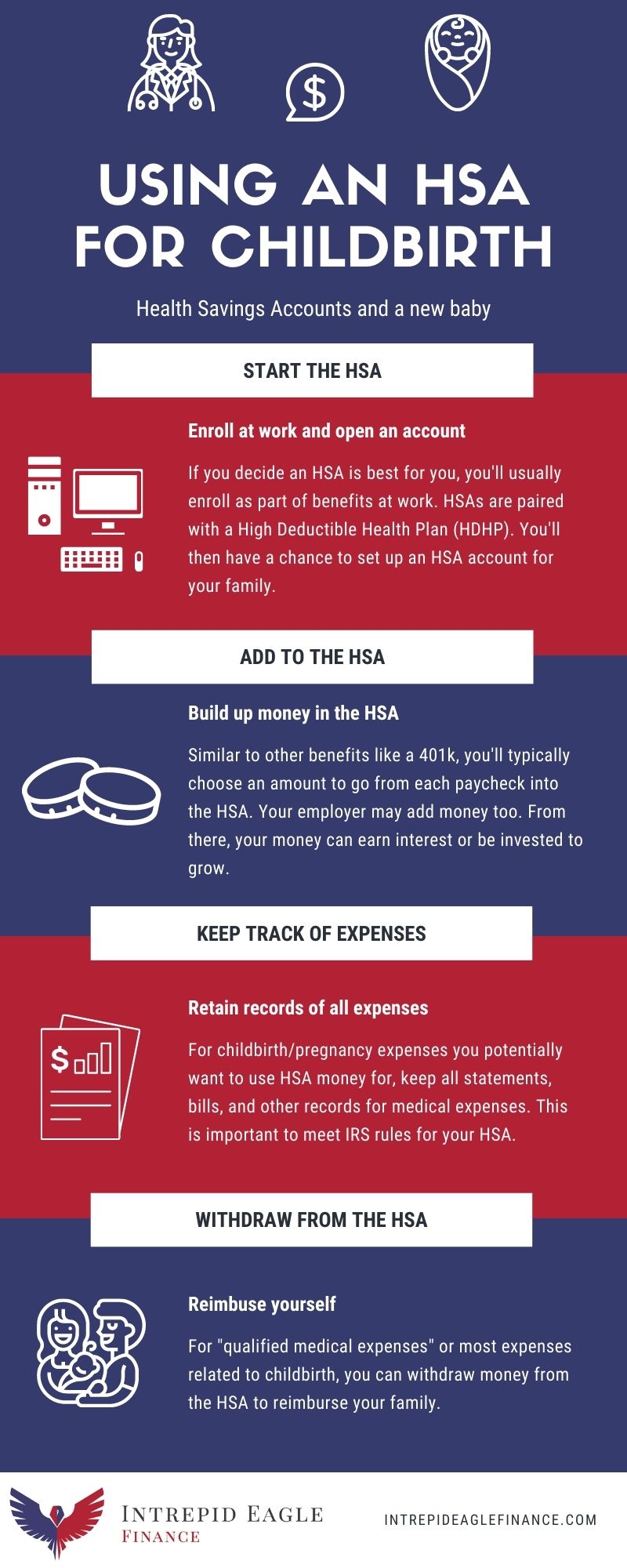

A Health Savings Account is a kind of account you can have if you also have a type of medical insurance plan designated as a High Deductible Health Plan (HDHP). For employer provided health insurance, your employer should let you know if you are eligible for a HSA. The idea behind an HSA is you put money into the account on a regular basis and then withdraw money later when major medical expenses arise. HSAs are unique types of accounts because they are “triple tax free.”

When you contribute to an HSA, you receive a tax deduction. While money is in an HSA, if it earns interest or grows, you pay no taxes. Later on, as long as you withdraw the money for what the IRS deems a “qualified medical expense”, you pay no taxes then either. Although, keep in mind the HSA is used to cover what insurance doesn't or what is known as “out of pocket expenses”.

Can an HSA be used to pay for childbirth?

The IRS maintains a list of qualified medical expenses, but almost all expenses related childbirth are eligible. This includes expenses like delivery of a child, medications (epidural), C-section, and more. Because the HSA covers your family as a whole, this includes expenses specific to Mom and/or the baby. As with anything involving the IRS, there's more to it. Keep reading for more on how to approach this question.

Examples of Expenses that can be reimbursed with an HSA

Each of these has requirements and stipulations from the IRS. Verify your situation is eligible before taking action.

- Breast pumps and lactation supplies

- Doula fees

- Fertility Enhancement (includes in vitro fertilization)

- Hospital Services

- Certain Insurance Premiums

- Lab Fees

- Lodging

- Meals

- Medicines (Such as epidural)

- Midwife

- Surgery

- Some Transportation Costs

How to save in an HSA to pay for a baby

Most people who have an HSA do so through work. If you’re in that boat, then your employer will help you set up an account. In the HSA account, you may have the option to choose investments or other ways to grow your health care dollars. As for putting money in, employer-based HSAs make it easy by allowing you to deduct money out of each paycheck. This is generally something you set up during benefits enrollment but can also adjust during the year.

Spread the cost over multiple years

Welcoming a new child, even with “good” insurance, comes with a large bill. Saving in an HSA can help break the cost up over several years. How? Let’s say you and your spouse are planning to have a child in two years. You estimate the amount insurance will not cover to be $6,000. You decide to save $2,000 this year and next year in your family’s HSA. In the year your new child is born, you put another $2,000 into the HSA. After you’re back home with Mom, Dad, and baby, you withdraw money from the HSA to cover the cost of your new addition. Would you rather have set aside $2,000 during a single year (three years in a row) or have a bill for $6,000 show up and be liable all at once?

Use Your HSA for other Pregnancy Costs

We tend to focus on the arrival your new child for the cost question. That's with good reason since that's the time some of the largest bills arrive. You can use your HSA to help with costs that arise during the pregnancy as well. This includes items such as visits to the OB-GYN, prenatal vitamins, pregnancy tests, prenatal ultrasounds, prescription medicine, and some physical exams. This is just a sample, so be sure to do your research before assuming an expense does or does not qualify.

Pregnancy Tests, prenatal vitamins, and OB-GYN visits long before baby arrives are all eligible for HSA expenses.

Things to remember for your HSA and baby plan

It’s important when you withdraw money from an HSA to keep excellent records. In the event you are ever audited, the government will ask you to prove money taken from an HSA was used for qualified medical expenses. It’s a good practice to keep a file with all medical bills and receipts during a given year. The IRS wants to know when money goes into or out of an HSA. Be prepared to answer that question as part of filing your taxes. Also remember that the rest of the family has health care needs as well. If you’re deciding to fund an HSA, account for those needs also.

Money Mistakes Expectant Parents Make (and how to avoid them)

We help Christian families on their journey to financial freedom. If you would like more posts from us on how to balance what's truly important with your finances, please sign up for our free newsletter. If you’d like to hear more about how Intrepid Eagle Finance helps families manage their financial lives, click here to learn more and schedule a free consultation.