Why Paying Off Your Mortgage Early isn’t Always the Best Priority

Some families, when they get a bit of margin or “extra” each month, consider paying down their mortgage. Your home loan, which is probably one of your largest recurring bills, is something many households would love to eliminate. Is paying down your home mortgage the best decision you can make?

Think About Financial Decisions on a Spectrum

Before you dig into decisions about your home mortgage or any other financial decision, it’s a good idea to think about how we make financial decisions as a whole. Let’s say you see a friend of yours decides to stop to fill up their car. They decide to stop at station A. It turns out station B across the street has gas for 2 cents less per gallon. Did your friend make a good decision or a bad decision? Perhaps, instead of a good or bad call, it just wasn’t the optimal decision.

Few financial decisions are just black and white or good and bad. Are some better than others? What if your fuel-seeking friend has a gift card or discount at the gas station they choose? Would your opinion then change?

"the best possible; producing the best possible results" Optimal as defined by the Oxford Learner's Dictionary

Ideally, you want to make the most optimal decision for your family in terms of financial questions. Optimal financial decisions are often unique to your family. It's not always possible to make the most optimal financial decision, for one reason or another, but that’s the goal. Now, where does paying down a mortgage land on the spectrum and why?

Find out what financial questions to ask in your family

Weigh the Alternatives

If your family is considering paying more than the required amount for your mortgage every month, we’re assuming that you have funds beyond your regular monthly obligations. If so, that’s great. Unfortunately, many Americans can’t say the same. With that monthly margin, there are a multitude of beneficial financial decisions you could make. Some could be spending, others could be for financial goals, or any combination under the sun. Financial goals could include things like investing for retirement, save for college, adding to an emergency fund, or paying down debt.

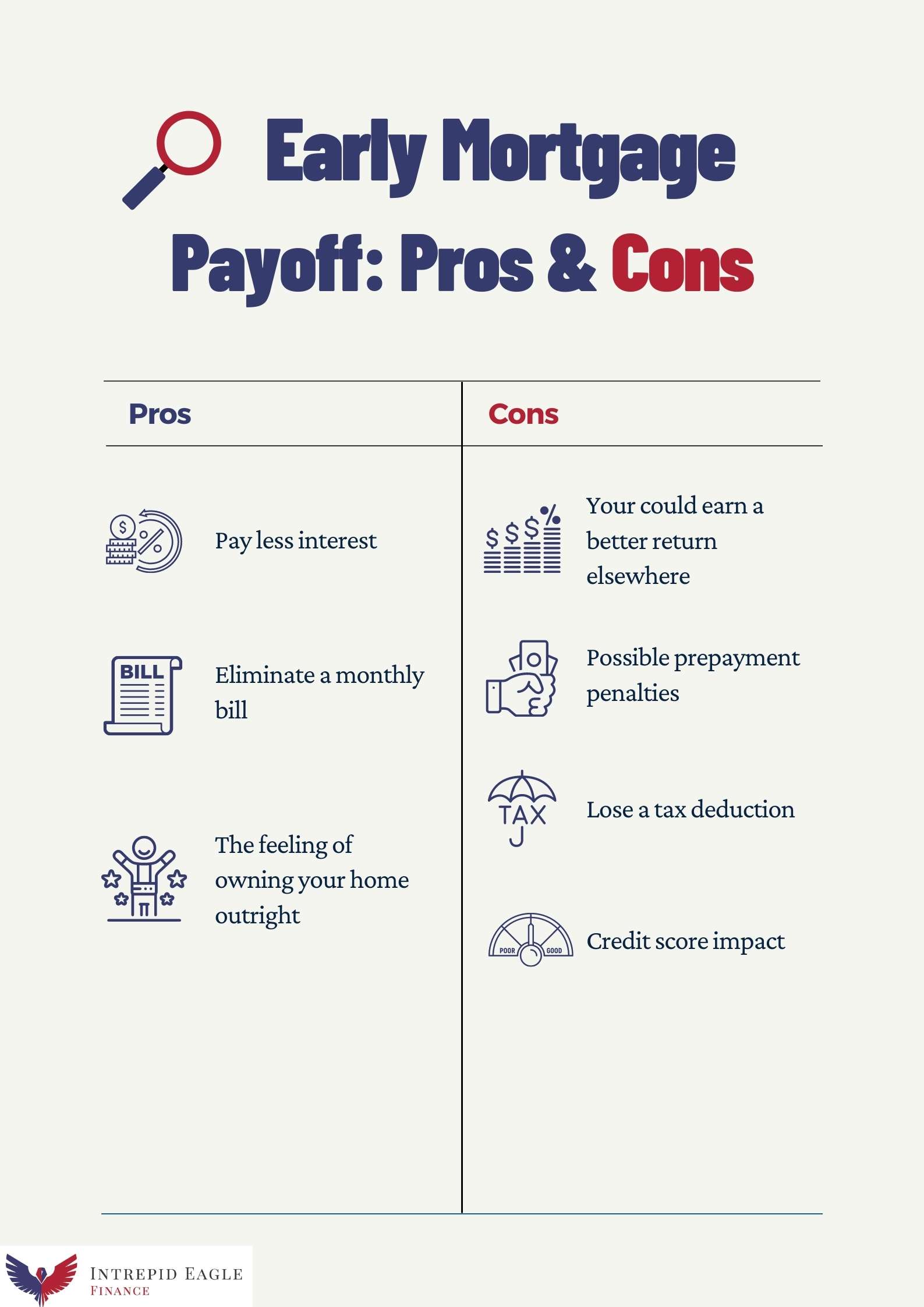

The Pros and Cons of Paying Off Your Mortgage Early

Pros of Paying of Your Mortgage Early

Pay less Interest

As with any loan, each month’s mortgage payment consists of principal and interest. If you pay off a 30-year mortgage in 20 years, then you avoid the interest you would have paid over the final 10 years of the loan. How much you save on interest payments is dependent on when you pay the loan off and the terms of your mortgage such as interest rate, length of loan, and other factors.

Eliminate a Monthly Bill

You can’t eliminate your water bill, but you could potentially eliminate your monthly mortgage payment. This benefit is one of upsides most cited when families consider working on an early mortgage payoff. Most family budgets have their house payment as either the largest or one of their largest recurring bills so the prospect of eliminating that regular obligation is attractive.

The feeling of owning your home outright

One of the more intangible reasons given when families say they want to payoff a home loan early is to own their home with no claim from a bank. The idea is that many families feel because they owe money to a lender then the home is not completely theirs. The potential peace of mind that comes from removing this obligation is something some families want to have.

Cons of Paying of Your Mortgage Early

You could earn a better return elsewhere

As an alternative to paying more than your required monthly mortgage payment, you could decide to invest the money. Since 1926, the average annual return of a diversified stock portfolio has averaged around 10%. Since most mortgages (interest rates) are quite a bit below that, over the long term it would be likely for invested money to perform better than the interest savings you would get. Over the short term, that would be much more difficult to gauge since investing is most appropriate for those who can dedicate money over a long period of time.

"the profit from labor, investment, or business" Return as defined by Merriam-Webster

Possible Prepayment Penalties

Banks and other mortgage providers make money by charging interest on loans. One of the ways they protect themselves is by using prepayment penalties on some loans. You could have a mortgage with a prepayment penalty clause. This means that when you make an extra payment to pay down your loan principal, the loan provider could charge a fee to do so. Some mortgages with this sort of penalty/fee reduce or waive the fee after time passes. For example, the fee could be more in the first year of the mortgage than the second year.

Prepayment penalties are regulated and, in some cases and/or states, are not allowed at all. It’s important to check with your current loan servicer to know the specifics of your loan. If part of your extra payments are eaten away by penalty fees, then the impact of your efforts are immediately diminished.

Lose A Tax Deduction

Part of the federal tax code allows your family to potentially use the interest paid on your mortgage each year as a tax deduction. How does a tax deduction help? A tax deduction helps reduce the amount of your family’s income that gets taxed. That could help your family pay less taxes or possibly receive a larger refund in some cases. While it rarely makes sense to do something just for a tax deduction, it is worth noting that a mortgage is the only type of loan you can have that potentially helps reduce taxes.

What is a tax deduction?

Credit Score Impact

It may sound strange, but an early mortgage payoff can negatively impact your credit score. It’s counterintuitive, but the credit reporting bureaus will sometimes lower your FICO score when a home loan is paid off early. Why? Credit scores are a combination of many factors. Some of the factors that could be impacted by an early payoff include payment history, credit utilization, length of credit history, and/or credit mix. One or a combination of those criteria from the credit reporting bureaus could lower you or your spouse’s credit score.

Credit scores affect the terms you are able to secure for future loans. Outside of loans, a less than optimal credit score can have other negative effects on your family. Tasks like applying for a new job, signing up for utilities, insurance rates, or getting a cell phone can all be more expensive and difficult with a lower credit score.

Be Careful About Being House Rich and Cash Poor

House rich and cash poor is a situation some families unexpectedly encounter when they make an early mortgage payoff a priority. Sometimes called asset-rich-cash-poor, the idea is a family may own a significant portion or all or their home on paper but then find themselves in a situation where they are short of cash for things they want or need. How could that happen?

Think about a family with young children who wants to payoff their 30-year mortgage over the next 15 years. They then find when their oldest starts college they own a large asset, their home, but have not set aside enough for college tuition. The lack of a mortgage payment helps, but they still find covering higher education (tuition, room & board, books, supplies, etc.) difficult. Is house rich, cash poor a problem for everyone that pays off a home loan early? No, it’s not, but it’s important to keep an eye on the entire picture and balance goals to make sure adequate cash flow at the right time is not a problem if you decide to pursue extra mortgage payments.

Why is it Better [Sometimes] To Not Pay Off Your Family’s Mortgage?

Assuming you have money each month to put toward extra mortgage payments, what else could your family potentially do with that money? Here’s a few possible paths.

Non-Mortgage Debt

If you have other debt beyond a mortgage, think about paying that debt down first. Why? Mortgages are typically the lowest interest rate you will get when your family gets a loan. Credit cards, auto loans, student loans, and others are likely at higher interest rates or less favorable terms. Your home loan also carries a potential tax benefit these other loans do not.

Education Savings

The price of college continues to rise. One of the ways families with college hopeful children can prepare is by setting money aside over time to cover the cost of tuition, room & Board and other higher education expenses. When you use an option like a 529 Education Savings Account, your family can save and grow money over time to help avoid stress when it’s time to pay the first tuition bill.

Investing for Retirement or Other Goals

Retirement may seem far away when you are raising a family. This is counterintuitive, but the further away from retirement you are the easier it is to pay for. Why? The magic of compound interest. The longer you invest money, the more compounding will work so you don’t have to. The longer you wait, the more work you need to do to make up for lost compounding time.

Some families resolve that they’ll get started on investing for something like retirement after the mortgage is paid off. As you weigh that decision, consider what you might give up as part of the cost.

Home Improvements that Carry a Financial Benefit

If you still want to focus on your home, consider home improvements that will help reduce recurring costs at home. Think about projects like redoing old insulation, getting a smart thermostat, updating old heat pumps or water heaters, and other improvements that can help with costs like utility bills

How to Cut Your Home Energy Bills

Is Paying Off Your Mortgage a Good Idea?

The answer is it depends. Is paying off your mortgage early a good idea? Yes. Is paying off your home loan early the best idea for your family? Likely Not. Because of the factors discussed above, using extra money to pay down your mortgage principal is not the optimal choice for most families. Is paying off your mortgage early a bad idea? No, but it may not be the best idea for your family. Keep this in mind as you strive to make the best and wisest decision for your family finances.

"For which of you, desiring to build a tower, does not first sit down and count the cost, whether he has enough to complete it?" Luke 14:28 ESV

What if We Still Want to Pay Down Our Mortgage Because it “Feels” Right?

Watch out for financial decisions that are made solely on what has a good feeling. With that said, if you still want to pay some extra on your mortgage each month it doesn’t have to be all or none. Let’s say your family has decided that you have $50 each month to allocate somewhere. In lieu of an all or none decision, how about allocating $25 toward your mortgage goal and another $25 toward retirement savings? Don’t box yourself in with decisions that seemingly offer just one path. Instead, think about balancing different goals for your family.

Summary

As you and your spouse weigh this decision, keep in mind your overall family financial priorities. Your family is unique and so are your priorities. Take care to discuss the pros and cons of where to direct extra funds each month. When in doubt, pray about it and think about getting some help to make the decision.

We help Christian families on their journey to financial freedom. If you would like more posts from us on how to balance what's truly important with your finances, please sign up for our free newsletter. If you’d like to hear more about how Intrepid Eagle Finance helps families manage their financial lives, click here to learn more and schedule a free consultation.